Credit Card Comparisons

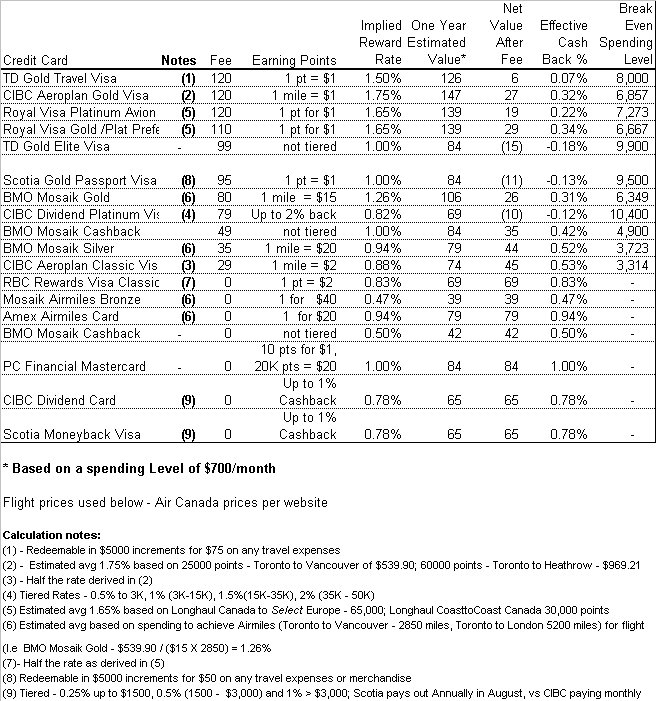

I've had a number of comments a few posts back on credit cards and the different rewards that they offer. I decided analyze what I think are some of the more commonly used credit cards. While I've analyzed 18 different cards, I am sure this does not cover all of my readers' cards. While your individual card may not be covered below, I believe that the message will be the same. You must spent a lot of money for these cards to be worthwhile.

I've based the analysis on my average monthly credit card bill spending of $700. For each card analyzed I have also indicated a break even spending level. If we take TD's Gold Travel Visa as an example, an individual would need to spend $8,000 just to cover the cost of the annual fee.

There are a number of limitations with the analysis.

- I've excluded interest rates on the cards, since I pay my bill every month

- The analysis excludes differences in the cards such as insurance coverage, flight change options, upgrade options, waived banking fees associated, free auto clubs with a particular card etc. While these may be very valuable to a frequent flyer, I feel that for the average consumer they are useless.

- The analysis ignores booking limitations such as must have a Saturday stayover or must be booked 14 days in advance

- Since many of the cards use a point system, I determined an implied rate using Air Canada flight prices published on their website. I took 2 September flights: Toronto to Vancouver($539.90) and Toronto to London, UK($969.21) as my base fare price and used these prices to calculate an average implied rate.

How do your cards rate? My vote would be for the PC Financial Mastercard or the CIBC Dividend Card. While one reader pointed out that Loblaws is expensive and therefore the rewards for the PC card may have a lower value, No Frills is a cost-effective grocery store where points can be redeemed. I also rank the CIBC dividend card higher than Scotia's Moneyback card because of the monthly payouts vs Scotia's annual payout. Some of the other cards do have a higher rewards rate, but I personally prefer cash/near cash(groceries) than a travel reward.

posted by Frugal Canadian @ 8/06/2006 06:47:00 PM

13 comments

![]()